MLB’s Cynical Spreadsheets

Skinflint Owners, Moneyball Manipulators, And The Duty To Give A Damn

There is an epidemic among baseball owners and in many ways it serves as a microcosm for American business (and politics) generally: how much can we strip away and sell off from the essence of a thing, how much quality can be diluted in the name of efficiency—the term itself frames negation and subtraction as necessary positives—while selling to the consumer that this is in fact better for them. In the name of efficiency we use AI to plagiarize and regurgitate the dwindling writers who think, report, create. In the name of efficiency we maximize present profit while long term planning is met with a sneer, unless it comes bearing an optimization model.

What, in short, can the 21st Century masters of the universe get away with?

In Major League Baseball this epidemic manifests in owners buying (or, too often, inheriting) teams and running them like a leveraged buyout asset, a page in a portfolio spreadsheet where the calculation is not about pursuing durable greatness from which profits both financial and spiritual will follow, but rather about squeezing every present-day penny from the margins.

The pursuit of profitability in baseball is decoupled from excellence for many reasons, not least of which is special legal status allowing for almost communistic revenue sharing paired with mid- and even some large-market franchises co-opting the success of analytically-driven small market teams and selling the efficiency lie to their fans; i.e., the Moneyball effect.

The end result: a majority of MLB owners skulk around in the shadows like parasites, collecting guaranteed millions in revenues and profits while refusing to spend money on even one star-level player—thereby ensuring the club is less popular and less valuable—then having the gall (and complete lack of awareness) to complain about the spending of the few teams that drive the entire industry and make their own businesses viable, if not relevant.

Owners like Detroit’s Chris Ilitch.

Ilitch and his ilk, assisted by a new generation of MBA-dazzled execs, actively bastardize and misrepresent Moneyball’s lessons—as the subtitle spelled out, the yin to uber efficiency’s yang was creative management and, duh, winning—but savvy investors are putting the lie to the idea that sports ownership is not profitable.

The irony is actual private equity folks seem to better understand sports teams’ special value and profitability—they are putting money in, while many legacy owners seem to misvalue these coveted community artifacts and run them as if eyeing a quick flip profit. They annually repeat the same clumsy process of slashing payroll costs and collecting corporate welfare; the flip never comes.

To be fair to all, many cheapskate owners are not even pretending to be concerned with efficiency. Some are simply incompetent, craven, and/or greedy; call theirs the DGAF model.

A phrase you will hear often around baseball discourse is “the game is getting younger,” as if decisions to aggressively promote prospects—many of whom are not at all ready for the big show—over signing All-Star caliber free agents is born of a desire to make the product better and not simply a way to reduce spending, profit in the margins, and perennially sell hope (stop your clamoring, plebes, can’t you see we’re close!).

The “we’re close” excuse is perfect because, as anyone who’s been on any social media site or frequented a sports bar knows, fans tend to side with their teams over individual players, even when hoping their recalcitrant owner will make a move. Sure, he’s a four-win player but I don’t want us holding the bag for those last two years. Sports owners have reprogrammed fans—we all want to play GM or owner ourselves, after all—to view player pay as an adversarial, zero sum game that necessarily reduces something else, some vague future, and to see the owners’ self-imposed, arbitrary budgets and caps as immutable law. Voting against our own interests by another name.

We aren’t cheap we’re SHARP.

This cynical approach has been aggressively sold by the Tigers under Chris Ilitch, who inherited team control when his beloved father, Mike, died in 2017. Chris immediately began slashing payroll. Aside from the monumentally misguided Javy Baez signing—which had enough red flags no truly sharp org would’ve done it—Ilitch has refused to spend on star level players. Not just free agents, either; he hasn’t shown a willingness to extend even homegrown stars from within.

A few years ago Ilitch hired Scott Harris as President of Baseball Operations. Harris, of course, has an MBA.

Ever since, Harris has relentlessly preached—and local media, necessarily locked in a symbiotic relationship to the team, duly regurgitates—a plan of “sustainable success.” In other words, my owner is breathtakingly cheap and has instituted a strict budget, but hopefully I can buy time with the public by pointing to the exciting kids we have in high-A. Buying time is antithetical to growing the business, but unfortunately MLB has created incentives that reward such laggards.

There’s a basic, fundamental problem with mid-market teams like Detroit relying entirely on the bastardized Moneyball approach, if we assume for a moment it is even posited in good faith: nowadays there are few competitive edges to gain via marginal efficiency and analytical savvy alone. The Dodgers and Yankees and Mets and Phillies are spending on talented free agents and loading up on analytics staff and processes and advanced facilities. They are at the vanguard of international markets too.

Beyond the futility of two-thirds of baseball pretending they’re the 2002 Athletics, there are existential and moral questions raised by a scheme wherein many if not most of the participants in a putatively competitive enterprise are not in fact competing.

What is the purpose of the league and its member clubs? Why does it exist in the first place? All the guaranteed revenues MLB teams vacuum in, the inexorable rise in valuations—where does that come from and why are you staked to it with almost no strings? Most importantly, if you own such a unique entity does it carry any special obligations along with the special benefits? Should it?

Just because you can run a baseball franchise like a distressed portfolio asset doesn’t mean you should.

And why not, says the stern capitalist, it’s just a business, wouldn’t a rational actor play it safe and risk as little as necessary, especially if the asset’s ultimate sale value rises regardless of on-field results?

First, trotting out a middling team year after year reduces the club’s value. More to the point, the answer lies in the nature of the business, the “why” that insulates it in completely unique ways.

Major American sports teams are not some widget maker or doomed dotcom created or acquired for the purpose of selling out or launching an IPO. The same web of tribal feelings that makes fans side with their teams over players, no matter how unsuccessful the team, is why owning a major sports franchise comes with special benefits no other business can dream of—exemption from antitrust laws and other regulations, along with hundreds of millions in guaranteed revenue and recession-proof growth—benefits that flow from a special status based on public trust and affection.

The usual market rules do not apply here. If you make a terrible television show no one is obligated to buy or broadcast or advertise it or watch it. It gets cancelled, quickly. If you make products that malfunction 60% of the time your business goes belly up (maybe not space rockets but you get our meaning).

Not so for an MLB team, who can readily fail like this and still profit. Win 43% of your games for seven years in a row? Seventeen years? Here’s $150 million and an amateur draft lottery ticket—ok, you can only get the lottery pick as a revenue sharing recipient three times in a row before taking a year off, then it resets; but the money never turns off. More grist for the hope machine.

Those rewards and many more, including psychological benefits, flow to an MLB owner because a baseball team is a different and distinct thing, an almost metaphysical extension of its surrounding community, with claims to its customers’ hearts and wallets that no random product or service can make. People are raised to care and root for and spend on the “lovable” (and even unlovable) losers. Sports teams are more like religious institutions than free market capitalist enterprises.

That’s why you get guaranteed revenue and legal exemptions in the first place; you are entrusted something that transcends the bounds of any old partnership, Inc., or LLC.

Those special benefits therefore should come with obligations: to make the team competitive, to generate fan excitement, to foster hope, real hope—in short, to win.

Or at least fucking try.

Instead, it’s become the opposite. Because we care so much, owners like Ilitch can do so little.

Five of MLB’s top six spenders made the 2024 playoffs, and three of the four LCS teams ranked first, second and third in payroll.

Winning requires spending, at least a little bit. Winning generates and sustains fan interest, which creates more revenue, which when reinvested makes the product better, which makes the club more valuable—which ultimately makes everyone richer.

The Tigers and The Ills of Ilitch The Younger

Perhaps no situation better exemplifies the Moneyball effect or DGAF model than the Tigers handling of homegrown star Tarik Skubal, who just won the 2024 AL Cy Young Award, and the team’s near-decade clawback of player payroll generally.

Skubal may simply be the best pitcher in baseball. He has been worth 12 fWAR since the start of 2022, a smidge more than Corbin Burnes—in 200 fewer innings. The seven pitchers ahead of Skubal in WAR during that time, and it isn’t by much, have each thrown at least 150 more innings than him. That’s how good he’s been on a per-inning basis. For most of the 2024 season he was the reason the Tigers were even given a passing thought by national media or fans of other teams.

And yet, according to a November report from Evan Petzold of the Detroit Free Press, the Tigers made Skubal an extension offer that was “not competitive” with the market for an ace.

Skubal will reach free agency in 2027, having trudged MLB’s long and Byzantine road of service time and arbitration-capped seasons for six-plus years, hence the extension talk (another benefit MLB owners receive: restraints on labor movement). It was even speculated the Tigers might trade Skubal at last year’s trade deadline; the team sold off other veterans, including their number two starter Jack Flaherty. An improbable hot final six weeks—coupled with some notable collapses (ahem, Twins)—found Detroit in the last AL playoff wild card spot, but team brass certainly weren’t planning to compete in 2024, even four months in.

Indeed every free agent they added last offseason was, like Flaherty, on short-term deals intended to resuscitate their value then flip them to teams actually trying to win something beyond the margins game.

So far this offseason the Tigers are following the same script, signing broken down battle horse starter Alex Cobb and defensively-challenged second baseman Gleyber Torres to one year, $15 million deals. They fill out the roster but are essentially flawed, potential trade bullets more than difference-makers.

And they’ve re-signed Flaherty to the biggest deal they’ve made since Baez, at $25M for 2025 with a $10M base in 2026 that can convert to $20M if he reaches 16 starts this year; it also has an opt out. This is a bit of a hedge; if he pitches great again, Flaherty will opt out. If he doesn’t they can find a way to not start him enough to owe him $20M.

There is nothing wrong with these deals in isolation, but they continue what is now an eight-year trend of Chris Ilitch behaving as if he cannot afford even one star player. This despite a clear need on offense and free agents like Alex Bregman available who would fill numerous needs.

Even that may be justified if you had a coherent strategy, let’s say to rebuild for a few years then strike at the right moment—as Luhnow did with the Astros. But that doesn’t track here: Detroit just achieved ahead of schedule yet now won’t pay a homegrown superstar? Skubal was making relative peanuts entering this, his second arbitration-eligible offseason. To wit, the reigning Cy Young made $2.65 million in 2024. He has made a total of $5.57M since reaching the majors in 2020. After the failed extension “offer,” player and team settled at $10.15M for 2025.

The Tigers are getting a massive bargain here. Skubal has been the most valuable pitcher in the game since returning from injury in the middle of 2023 (9.1 fWAR; Zach Wheeler is second at 8.0).

Many MLB front offices and agents use a WAR-to-dollars calculus when evaluating how to pay free agents. The current market assigns $11-12 million per projected win above replacement, per Eno Sarris.

Based on these parameters, Skubal was worth anywhere from $65-72 million in 2024 alone—a value to Ilitch of $60 million at the low end. Every projection system estimates Skubal will be worth at least five WAR in 2024. Ilitch is getting at least an 80% discount due to MLB’s arbitration structure.

To compare ace to ace, Gerrit Cole is making $36 million annually on a deal he signed in 2019. Skubal is better than Cole and younger, even at the time Cole signed (28 to 29). Wheeler recently signed a three-year extension at $43M per; he is 34. Skubal is just entering his absolute prime as a starting pitcher.

And yet, the Tigers make a “non competitive” extension offer to a player they drafted and developed, a player so good he kept a middling lineup afloat long enough to even make that late playoff run—Detroit went 21-10 in Skubal’s starts—a player who drew positive media and fan attention to the team for the first time in almost a decade, a player who is obviously the face of the franchise.

One way Ilitch could look at the situation: having just received $55+ million in present value from Skubal with no real intention to extend him (or lazily blame Boras, whatever), and just one, at most two more seasons to capitalize on his talents, we will instead invest in a star-level free agent hitter to give more bankable legitimacy to a team that, let’s be frank, got very fortunate in 2024 (Detroit ranked 21st in team offense by wRC+).

Instead, Ilitch pivoted to two one-year deals that are essentially minimum commitments, plus Flaherty which, it would not surprise us if the parsimonious strategy here is, we can trade Skubal and sell Flaherty to fans as the ace of our “sustainable success” roster.

Instead, the Tigers have watched a number of other affordable, good hitters sign elsewhere. Instead, they are reportedly “in” on Bregman but are also trying to “wait him out,” i.e. only if he’s cheap enough to win the margins game.

Just because you can doesn’t mean you should.

Of course the Petzold report was no surprise to Tigers fans. This Ilitch has been so penurious for so many years that many fans have largely lost hope he will ever make a significant investment in player talent. A popular Twitter baseball account run by a Tigers fan recently expressed this frustration in response to the team’s inactivity in the free agent market.

As Ice Cube once said, here’s what they think about you:

This new Ilitch era could not be a starker change for fans. The Tigers previous owner and Chris’s dad, Mike Ilitch, was a dedicated fan of the team and arguably its most beloved owner. A brilliant entrepreneur, Mike (and his wife Marian) began their business career by investing their modest life savings into a single pizza shop in a Detroit suburb. A few decades later, having built an empire of pizza franchises, he purchased the Red Wings, then the historic Fox Theater and other real estate in and around Detroit, and finally, the Tigers in 1992. For $85 million. We mention the Fox because the Ilitches were at the vanguard of restoring and rebuilding downtown Detroit. Mike understood the value and necessity to put something in to get something out, in business and beyond.

Mike liberally reinvested Tigers revenue into players for more than a decade in an effort to win a World Series, peaking at a nearly $200 million payroll in 2017 under a less lucrative national TV deal than the current one (which began in 2022). Under Mike’s expansive spending, the team had its greatest success since the mid-80s, winning the AL pennant twice and the Central Division four times from 2006-2014.

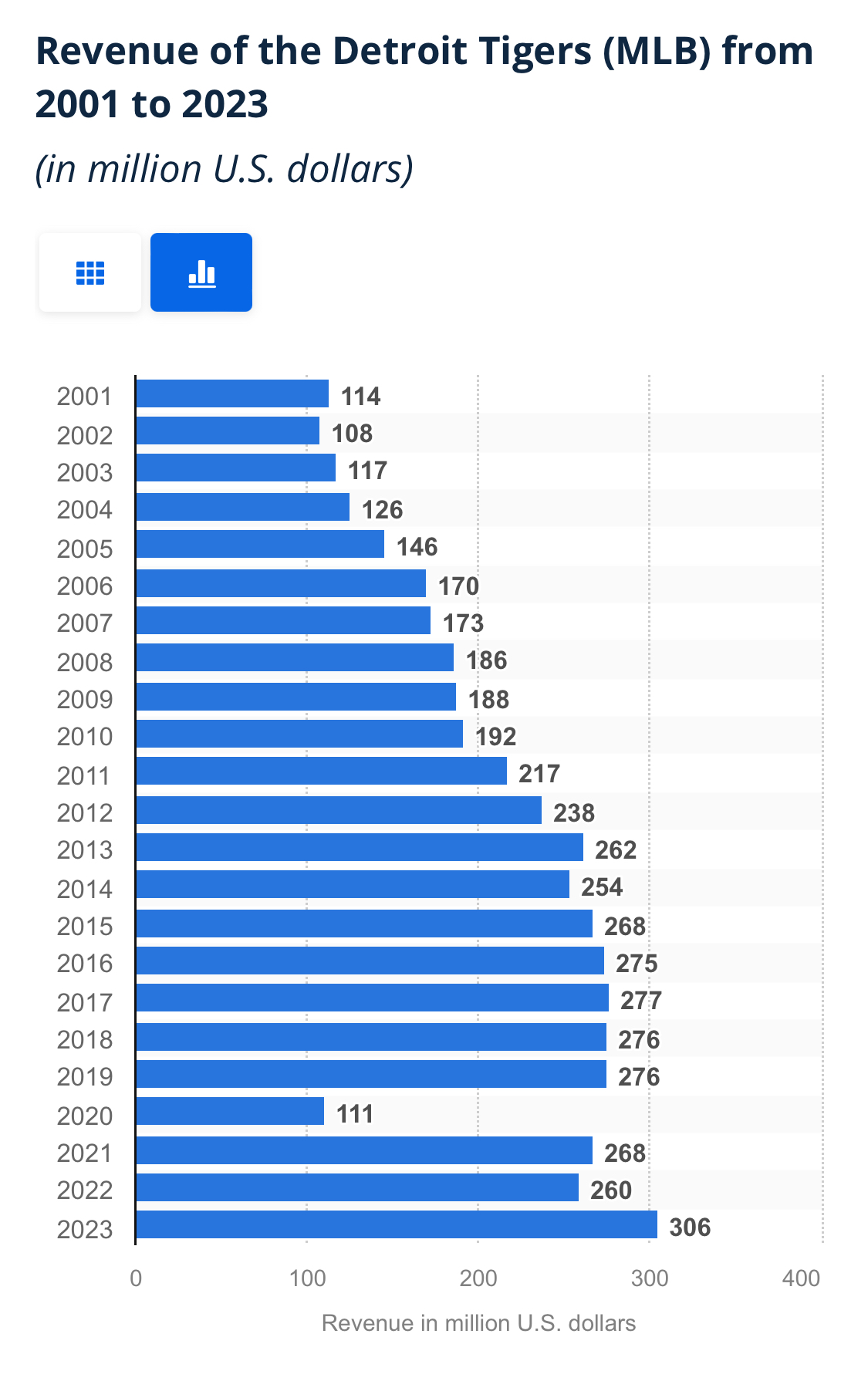

The elder Ilitch’s payrolls were regularly in MLB’s top five. Shockingly—the cold hard cash answer to “why try”—that era also generated a huge boost in revenue for the franchise (remember each team received approximately $30m more from national TV deals beginning in 2022, and 2020 was a lost pandemic year):

Data and image: Statista

After Mike died in 2017, Chris inherited control of the team and immediately began the process of cutting payroll. We are not arguing here that teams never will or should have down seasons or need a roster reset, but the Tigers have been bottom-10 in MLB player salaries for all but three seasons since 2017 and never top 15, with an uninspiring $97.6 million figure for the 2024 team, which ranked 25th (of 30).

Even after the Flaherty deal, the Tigers current projected 2025 payroll is $142M, per FanGraphs, which ranks… 18th. Again living in that band between 17-27th. Whenever Scott Harris has spoken this offseason he repeats his “sustainable success” mantra, pulling the “prospects really made an impact” card—while offering some vague suggestions that ownership will really really spend in the future. Maybe.

Alex Cobb and Gleyber Torres for $15 million, recycling Flaherty at a discount, and low-balling Skubal all put the lie to those claims in the near term. These Tigers are more vulture than apex predator.

Tigers beat writers duly repeat and amplify the team’s message—we are mining a more reasonable and careful tier, e.g. the speculation they might trade for Yandy Diaz (who is 33 and, you guessed it, on an expiring contract with just a team option for 2026). The beats are getting those ideas from the team and are dependent on it. We don’t blame them but the club’s intent is the same. It’s about reprogramming expectations.

The Tigers last won their division in 2014.

Just because you can doesn’t mean you should.

There Is ALWAYS Money In These Banana Stands

We have to estimate MLB team revenues, as despite very public player contract reporting rules, teams and the league are not required to open their books. MLB has new and extremely lucrative national TV deals totaling $12.7 billion over seven years; each franchise receives roughly $50 million from these annually. The Tigers receive between $40-50 million from their local TV deal. The league’s spendiest teams gave $500 million to their thriftiest brethren via revenue sharing in 2023. The Athletics for example received $70M last year—talk about falling up.

(We are not tackling the salary floor/cap solution to MLB’s payroll disparities here. Such a system would surely help, but does anyone doubt that owners like Ilitch or John Fisher would just do the bare minimum to get over any arbitrary floor? Would they need to be given more revenue sharing money to do so?)

Reports estimated Tigers revenue at $306 million in 2023, though it’s unclear whether that included any corporate sponsorships. (Some teams generate tens of millions and even more via such sponsorships. Teams with stars, anyway). Much of that revenue is de facto guaranteed; simply by being part of MLB even the lowliest franchise receives upwards of $150 million between national and local TV and revenue-sharing, before even considering gate and merchandise.

Once we add ticket sales, merchandise, licensing, and sponsorships, Tigers estimated revenue has recently sat in the $300M range. Yet payrolls have been a third or at best, 40% of that (the fact the books are closed and so closely guarded, as well as the private equity bros’ rush to invest in MLB, should have reasonable observers assuming actual revenues are higher than the reported estimates).

Harris will tell you Ilitch the younger has made important investments “behind the scenes,” to training facilities and processes and coaching and the team charter. This is Moneyball co-opting at its worst. In actuality, they want credit for making the most basic, necessary expenditures that every other team is also making. It’s like saying you remodeled your bathroom because you replaced a broken toilet, which you broke yourself.

The Tigers are hardly the only, or even most egregious, example of gaming the system for marginal profit despite immense potential. Miami is now the ninth-largest metro market and one of the most expensive places to live in the country; that franchise has been scamming its fans across three-plus decades, regularly residing in the bottom-five of payrolls. Ex-Marlins President David Samson has somehow birthed a media career! Recently speaking about the Jimmy Butler standoff with the Miami Heat, Samson said, “I wouldn’t trade him even if I got the package I wanted, just out of spite.” He wasn’t joking or exaggerating for effect—he has told similar stories about moves he made or didn’t make with the Marlins, with the intent to punish players, satisfy his own ego, or simply operate the organization as miserly as possible.

That is how some of these guys think. They are not trying to win. They are not even trying to run a competitive business, let alone a sustainably growing one. They are just skimming off the margins in a failsafe system supported by their communities and the teams that matter. Then they will turn around and complain of tepid local interest.

Pirates fans get it. Despite being one of MLB’s richest owners, Bob Nutting has been as penurious as they come. A 2022 Post-Gazette exposé revealed Nutting has directed that player payroll be strictly tied to ticket sales and concessions; all TV revenue, funds from revenue sharing, and merchandise and concessions margins are retained as net profits for Nutting.

Similar to the Tigers, you won’t be surprised to learn that the Pirates greatest success came from 2013-2015, when their payrolls were highest this century—and the only seasons they have made the playoffs in the last three decades (not that the payrolls were all that high even then). It’s gotten so bad with Nutting that state legislators commissioned independent studies on the team’s middling economic impact. They sent letters to the owner begging him “to improve the team and ensure taxpayers who helped fund the ballpark get a better” ROI. The study found “a positive relation between payroll and wins,” and between winning and local economic activity.

That was July of 2024.

The last time Pittsburgh signed a free agent to a multi-year deal was December of 2016.

Pirates ownership has also promised and failed to deliver aggressive free agency spending multiple times in order to weasel more county money to build and renovate PNC Park. Even after all the public funding, instead of naming the park after Roberto Clemente as fans hoped, ownership sold the naming rights to a financial services firm. High finance again!

Ilitch has also taken advantage of public funds. For example, Little Caesars Arena is owned by the city’s Downtown Development Authority but leased long term to Ilitch rent free; nor does the city receive any revenue sharing from concessions, parking etc. as it did with the Red Wings’ prior home. Public tax dollars covered 58% of arena construction costs and the State of Michigan granted Ilitch $250 million more in tax exempt bonds. This was all approved based on Ilitch promising $200 million towards a grand plan to develop new retail, residential and a new convention center downtown to “rival anything in the country”—none of which has come to pass.

That was in 2012.

Then there’s the A’s, the team that birthed the cynical spreadsheets in the first place: John Fisher—another failson inheritor—has already been investigated once for failing to spend the mandated 150% of revenue-sharing funds he received on payroll, and was in danger of another grievance for the same offense before a flurry of smaller moves nudged them just across the required spending line this year. Fisher of course also made the team as terrible as possible, negotiated like a terrorist against the city of Oakland, and did everything possible to get MLB to sign off on (and subsidize) relocation to Vegas (whose mayor has understandably not exactly embraced the notion of partnering with this slug).

The revenue sharing payroll spending mandate is in the CBA but the only mechanism to enforce it is an MLBPA grievance, so the players look bad or greedy when they hold skinflint owners to account. The league office has also rejected some prior grievances even though the owners’ math didn’t math (ahem, Nutting). Why is MLB itself not proactively enforcing this requirement, which would more “efficiently” improve the league as a whole?

Nationals, Orioles, Guardians, White Sox, Twins, Mariners, Reds. On and on it goes.

On the other end of the spectrum you had Peter Seidler, the recently deceased Padres owner. Like Mike Ilitch, Seidler was a longtime fan of the team who did everything possible to make them competitive; approving trades for Juan Soto, Dylan Cease, and Manny Machado, extending Machado and homegrown superstar Fernando Tatis Jr. Read any story about the Padres and one sees the entire organization—squabbling new owners excluded perhaps—driven to win for him. The community is engaged with the team at hitherto unknown levels. After the Tatis extension, home ticket sales went up by 9,000. Per game. In just a few years the Friars went from also-rans to true Dodgers challengers. Seidler will be a legend in San Diego forever.

You see, Chris Ilitch, that is what you could be.

Or you could be dirty Nutting or Samson.

Although treated as immutable law, it is in fact a choice to say, well these are the revenues and they are capped hence we must operate in the margins. This overlooks a fairly obvious truism of any business but especially baseball: the most direct way to increase revenue is to make the product/team great and worth buying, as Mike Ilitch and Seidler understood.

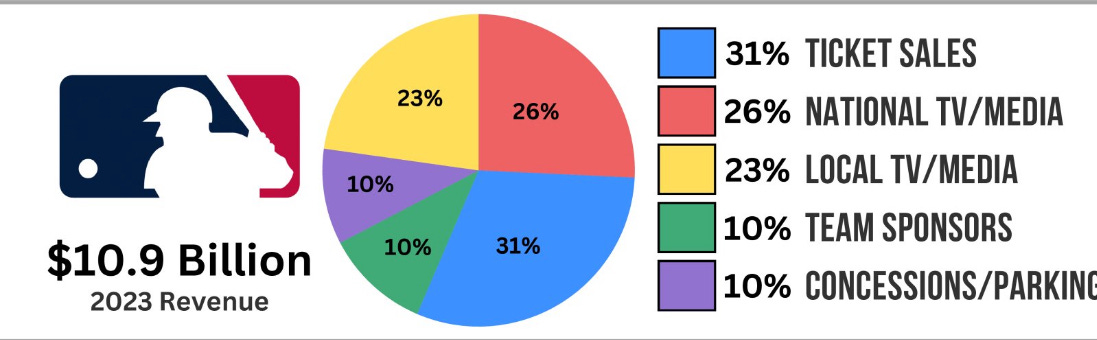

MLB teams derive a larger share of revenue from ticket sales than any other source, more so than the other “big 4” US sports:

^Image and data by Brooksgate

This is no surprise but it’s still stark: during the years Mike Ilitch was running top 10 payrolls, the Tigers averaged over 30,000 fans per home game almost every season. Relatedly, Tigers revenue peaked (relative to inflation) when they had stars and regularly threatened to win the pennant.

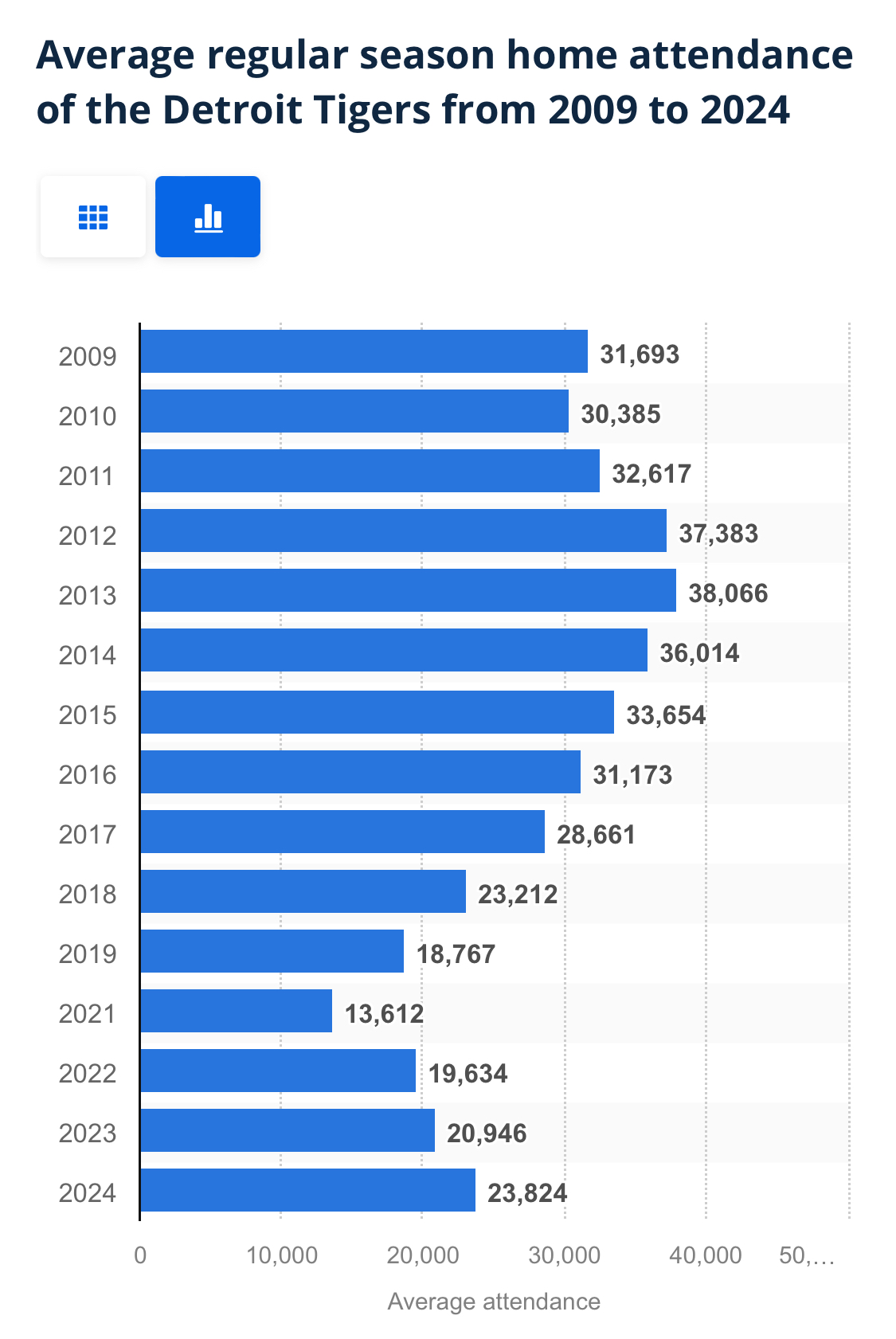

Once Chris Ilitch drastically cut player investment, attendance was nearly cut in half (even before the pandemic) and has never recovered:

Data & Image: Statista

Look at the damage to fan interest and investment. That is multiple years of 10,000+ fewer tickets sold per 81 home games. Even last season’s miracle playoff team averaged 14,000 less than the peak years of last decade. Some rough back of envelope math tells us the Chris Ilitch Tigers lose anywhere from $30 to $45 million annually in gate, merchandise, and concessions revenue relative to Mike’s “unsustainable” payroll teams. But Chris has done his own math and decided ~$50+ million in revenue sharing dough is a net-net win. For him.

Remember this the next time some sad-eyed owner or exec with an anonymous roster claims they don’t have the money to compete and the fans don’t support them, etc.—there is clear self-fulfilling prophecy at work when creating the conditions of failure then lamenting said failure.

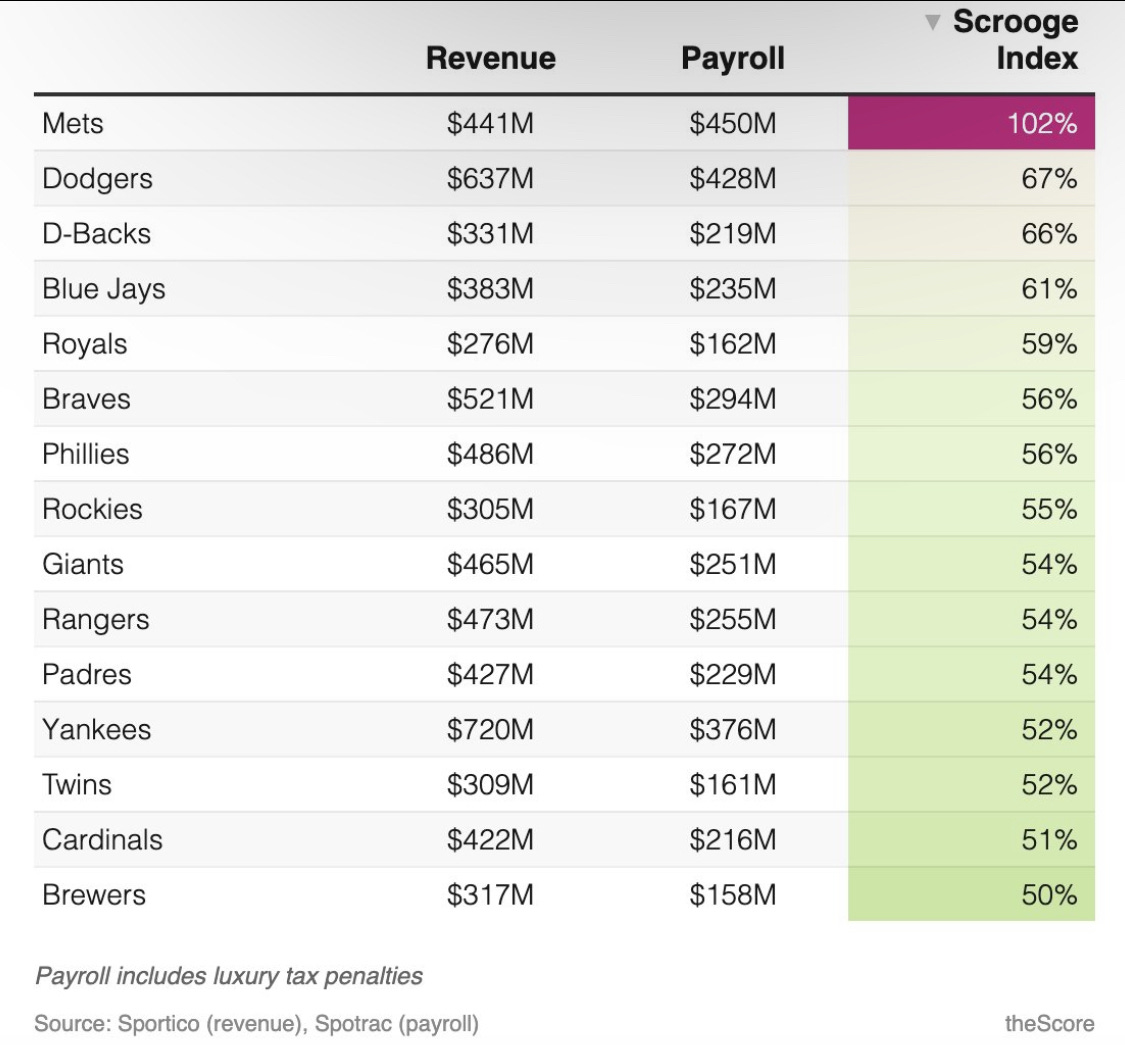

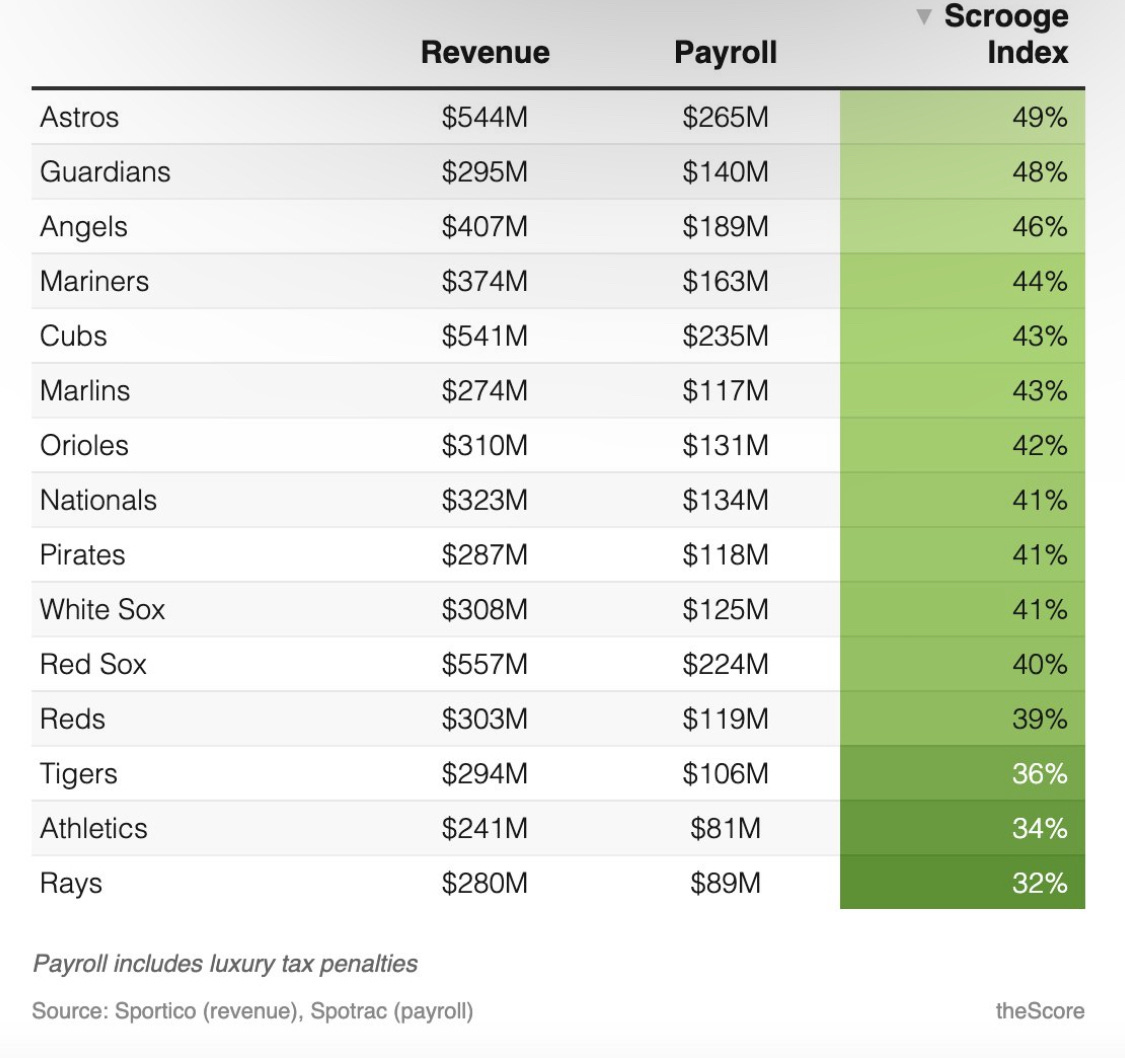

People get quite exercised about the Dodgers and Mets spending princely sums and assembling all star teams. Yes, they have advantages in gross revenue but here’s the thing: those organizations plow more money back into the team as a percentage of revenue than others too:

Scrooge Index by Travis Sawchik, The Score

Note the D’Backs. Phoenix is a comparable market to Detroit but they are absolutely going for it, having just added free agent Corbin Burnes for six years, $210 million. More on that anon.

Meanwhile the Tigers? Not only are they running objectively low payrolls, they have also been skimping relative to the revenues they do have. (It’s the usual suspects in the bottom 10, plus the Red Sox, who at least had been much higher in payroll in the years preceding 2023).

This is not an issue of lacking a way. Chris Ilitch and, frankly, most of MLB’s owners lack the will.

It is especially instructive when the Mets and Dodgers plow the highest percentage of baseball revenue back into player pay. We have levied the VC- or consultant-ball allegation at the Tigers but ironically, the Dodgers are owned by a financial investment firm (Guggenheim Partners) and the Mets by Steve Cohen, who made his vast fortune in hedge funds. There may not be a better poster boy for the uselessness of high finance than Cohen (who allegedly benefited from practices Christopher Moltisanti would admire and the SEC decidedly did not), but his behavior as Mets owner is both morally good and economically rational.

The irony of course being these entities that specialize in cynical spreadsheets and maximizing marginal efficiencies believe that spending on the team is the best way to increase franchise revenues and overall value. Guggenheim isn’t spending on a whim; the Dodgers could be less competitive and still come out way ahead. No, they spend on players because there is an economic incentive to do so. A better product is easier to market and to sell at a higher price, whether that be tickets or parking or TV deals or corporate promotions—or cashing out of the entire asset.

MLB’s financial health has never been better. The league recently announced 2024 revenues of $12.1 billion, a record and 4.3% increase over 2023. Adjusted for inflation, revenues have grown 15.2% since 2012 ($7.5B). So in gross terms revenue is up almost $4 billion. Those reported league gross revenues do not include certain assets, including team-owned RSNs and other, franchise-specific holdings; there are more growth opportunities if an owner pursues them.

Chris Ilitch (and every owner today) has a number of revenue advantages his father did not: more national TV money, uniform sponsor patches, gambling partnerships, and a stadium sports book to name a few.

Also: access to private equity money. Lots of it.

Private Equity Bros Understand Sports Teams Are Bulletproof Growth Assets

Call me a foolish dreamer, but it’s pretty obvious that, salary cap or no, every MLB owner can afford at least one if not two All Star-ish players, whether by extending from within or via free agency. You can tell me about operating expenses and margins and I would ask you why smart money is trying to get in to professional sports ownership if it is so unprofitable.

Investor behavior is illuminating when the books are closed on privately-held companies.

PE firms are rushing into sports team ownership, including baseball since MLB allowed such investments in 2019. Clubs can sell any fractional ownership amount they wish to PE firms up to 30% of franchise control (the cap per investor is 15%).

Arctos Partners LP is the most notable such outside firm; it raised $4.1 billion in new funding for sports ownership investing in April 2024 and has an estimated $8 billion under management dedicated only to this market; they do nothing else. Arctos already has stakes in the Dodgers, Red Sox, Astros, Padres, Giants and Cubs in MLB alone. According to Pitchbook, 18 of 30 MLB teams have either direct PE investment or ownership stakes held by PE-affiliated individuals.

Surely PE firms would not be doing so if they believed the baseball business required nip and tuck accounting maneuvers just to break even every year, as owners like Ilitch might claim. And they don’t believe that. The Arctos website states: “sports are growth assets with compelling financial and operating performance… There is a significant opportunity to provide liquidity and growth capital to a historical inefficient market.” More efficiency!—followed by an uplifting Nelson Mandela quote about sports uniting the world, because of course.

Yes, they’re marketing something here but the liquidity point is indisputable. Arctos is not the only such firm: MSP Sports Capital, Redbird and Clearlake are among numerous other sports-focused PE firms while Ares, Silver Lake and Sixth Street are but a few diversified funds with sports arms.

No surprise, but investors like these are not financing losers or simply aiming for a long run payout. Arctos’ first sports fund is reportedly operating at a 45% IRR (internal rate of return), about 35% above the benchmark for funds in technology and media, per Pitchbook. These are not “quick flip” investments but they are not long term loans either.

Even staid big boys like Deloitte have a sports ownership investment division, and its website notes the benefits to team owners: “With valuations soaring in today’s market, owners may opt to sell a portion of their stake to capitalise on the top-dollar bids” PE firms provide while retaining a controlling stake—in other words, get a liquidity infusion and lose no control over the franchise.

The reasons for PE firms’ interest go beyond the bulletproof upward trajectory of the teams’ valuations. Their investor materials and research stress that sports teams’ valuations and profitability are “resilient” and “uncorrelated” to the broader market.

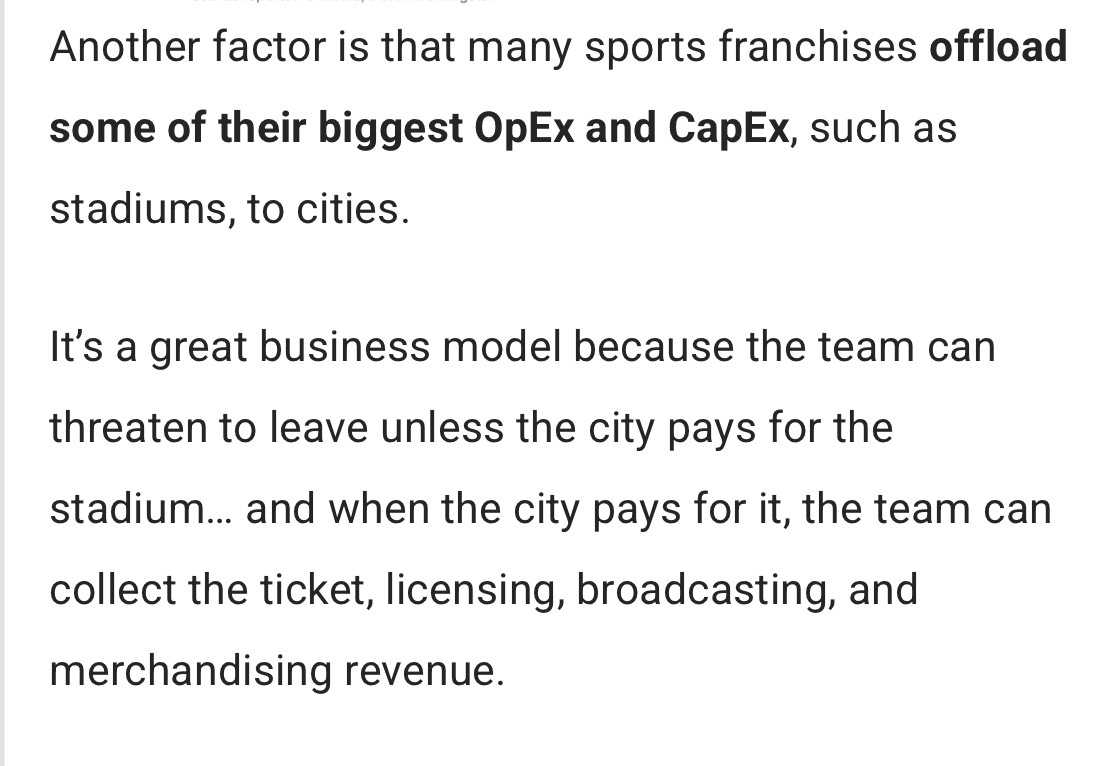

But why is that, what is the core reason? As we have intimated, sports teams retain value because fans spend on them through banking collapses, pandemics, Armageddon itself. Even when the team performs poorly. Moreover, sports teams create secondary business opportunities; fans’ emotional connections to their teams “function like moats for traditional businesses.” See https://mergersandinquisitions.com/sports-private-equity/.

That article cites myriad other reasons sports teams are attractive investment targets, including that many clubs are inefficiently run—low payrolls doesn’t mean you’re sharp—and, as we covered with the Tigers and Pirates, cities and counties often foot the largest costs that other businesses have to navigate themselves:

That’s how the sharks see it: clearly. Your widget company run with regard only to shareholder value has to bear its own capital and operating expenditures.

(One of David Samson’s great gambits was threatening to move the team to San Antonio, even setting up a photo op where he put on a cowboy hat and rode some poor horse around in a circle. The county eventually caved and financed a new stadium, the Marlins traded away their best players anyway, fan interest waned, and Miami-Dade residents are left with $2.8 billion in debt service.)

The other thread running through the PE investment trend is investors’ belief that sports teams are ripe for improved management processes and “unlocking new revenue.” Deloitte is diplomatically making the fairly obvious point that many clubs are pretty terrible (or lazy) at driving new revenue given a captive, dedicated and still-underdeveloped customer base.

PE firms offer another source of liquidity. Don’t want to sell off even 1% of your team’s minority ownership? Sixth Street invested in and now runs Legends, the sports concessionaire co-founded by the Yankees and Cowboys. As another example of a secondary liquidity deal, Sixth Street “invested nearly $380 million, for a 30% stake in Real Madrid’s stadium operations over 20 years.” Following that deal, the firm put in “roughly $540 million” for 25% of Barcelona’s La Liga TV rights over 25 years. The presidents of the two Spanish soccer superpowers spoke glowingly of these partnerships and the expertise the PE firm provided even beyond the scope of its investments. (Sports Business Journal, Alan Waxman profile, 7.29.2024 ).

Put another way, an MLB owner could partner with a firm like Sixth Street for a fraction of his club’s stadium ops and/or TV rights in exchange for tens if not hundreds of millions in liquidity, strategic ideas and operating advice, and still retain 100% control of the baseball club.

But wah we can’t keep up with the Dodgers.

Arctos’ co-founder and managing partner Ian Charles has spoken at length about why sports teams are so attractive, including on a podcast with Sam Kennedy of Fenway Sports Group, the entity that owns the Red Sox (link below).

They highlighted a few key points that could be the TL;DR of this entire column. Charles mentioned that sports teams have a “protected gross margin” (due to caps or revenue sharing) over “a long horizon,” i.e.: “Predictable profitability and very stable, underwritable revenue stream.”

They both stressed that the talent on the field and team competitiveness “drives everything else.” As Charles put it:

“Do fans and this community believe we are trying to put a superior product…on the (field), because then brands want to be associated with it.”

Are the PE guys white knights, angels? Certainly not; every situation is different. Red Sox fans may take issue with Kennedy and Charles’ stated focus on making the team as competitive as possible. On the other hand, Arctos has stakes in the Dodgers and Giants, two teams that have spent significantly (or tried to) on players recently.

The fact remains that the liquidity opportunity for owners is inescapable and sharp financial minds are eager to invest. PE firms with institutional investors do not chase losers. Teams can bring in tens if not hundreds of millions in cash flow without losing a fraction of a percent of franchise ownership.

If, like Chris Ilitch, you own an asset like this and can’t or won’t make it both satisfactorily profitable and consistently competitive, maybe you need to be doing something else.

Ken Kendrick Blows The Whistle On The Moneyball Scam

Ironically but unsurprisingly, Moneyball itself grew quickly from outsider strategy to mainstream business model, especially in the fields of data science and investment banking. The whole of America is a copycat league and folks love a new twist on making money. Penn’s Wharton School now has a “Moneyball Academy,” its premier on-campus program for recruiting—measuring Excel mastery instead of OBP—and hosts a “Moneyball Radio” program on Sirius. Beane himself taught a course on it at UC Berkeley’s Haas School Of Business. Theo Epstein, whose success made it fashionable for MLB teams to mine the Ivy League for exec brainpower, is a senior advisor to Arctos.

A 2020 ESPN story estimated that 43% of top baseball decision-makers hailed from an Ivy, up from just 3% in 2003. Former players-as-POBO had dropped from over 50% to 30%.

The bankers, nerds and baseball executives have converged.

Tigers POBO Scott Harris is the perfect grand vizier for this Ilitch in this moment. No former player, Harris is one of the many young MBA-toting baseball execs (Northwestern’s Kellogg), well schooled in the art of spreadsheet manipulation. One might observe that Harris is the hostage of a miserly owner. But he may be a friendly hostage, having been weaned on talent acquisition under Farhan Zaidi—B.S. in Economics, MIT and PhD in Economics from UC-Berkeley—who was so eager to show how smart he was that it often seemed he’d prefer to squeeze 27 home runs out of Wilmer Flores and Lamonte Wade than to add a major free agent to the Giants. Given this background, working for Ilitch may just make Harris as happy as a pig in the proverbial shit, mucking around for marginal values and touting the “sustainable success” mantra.

When we say Moneyball is being co-opted in service of a lie, we mean that many cheapskate owners—regardless of their actual market size, revenue or revenue potential—emphasize only one part of Moneyball’s lessons: ruthless efficiency through data. They sell the assumption that since Billy Beane’s approach was sound, in following it they too share the conditions which created that approach, i.e. the die is cast, their lot fated to play an “unfair game.” But the book’s other lesson, as highlighted by its subtitle, is the “art of winning” under budget restrictions via creative management and questioning prior biases.

The Tigers, Mariners, Pirates, Reds, Twins, Marlins, Nats—hell, even the Cubs and Yankees are crying poor—want you to believe that they are similarly situated to the 2002 A’s and to conclude that because efficiency is good, spending is an (unnecessary) evil. This feeds into that fantasy GM point: faced with signing a 4-WAR player to a multi-year deal as he finally reaches the open market at age 30, armchair execs can nod knowingly and cluck about the dangers of “eating the back end.” (Phrasing?)

Then Diamondbacks owner Ken Kendrick inadvertently (?) blew the whistle on his penurious colleagues.

Arizona is similarly situated to the Tigers: a relatively young team with upside that has tasted some playoff success but also had clear needs this offseason. The Detroit and Phoenix markets are almost identical in size too.

After trading for Josh Naylor to fill a hole at first base, observers believed the D’Backs might add a couple lesser pieces, most likely one of the cheaper closer-type relievers and a bench bat.

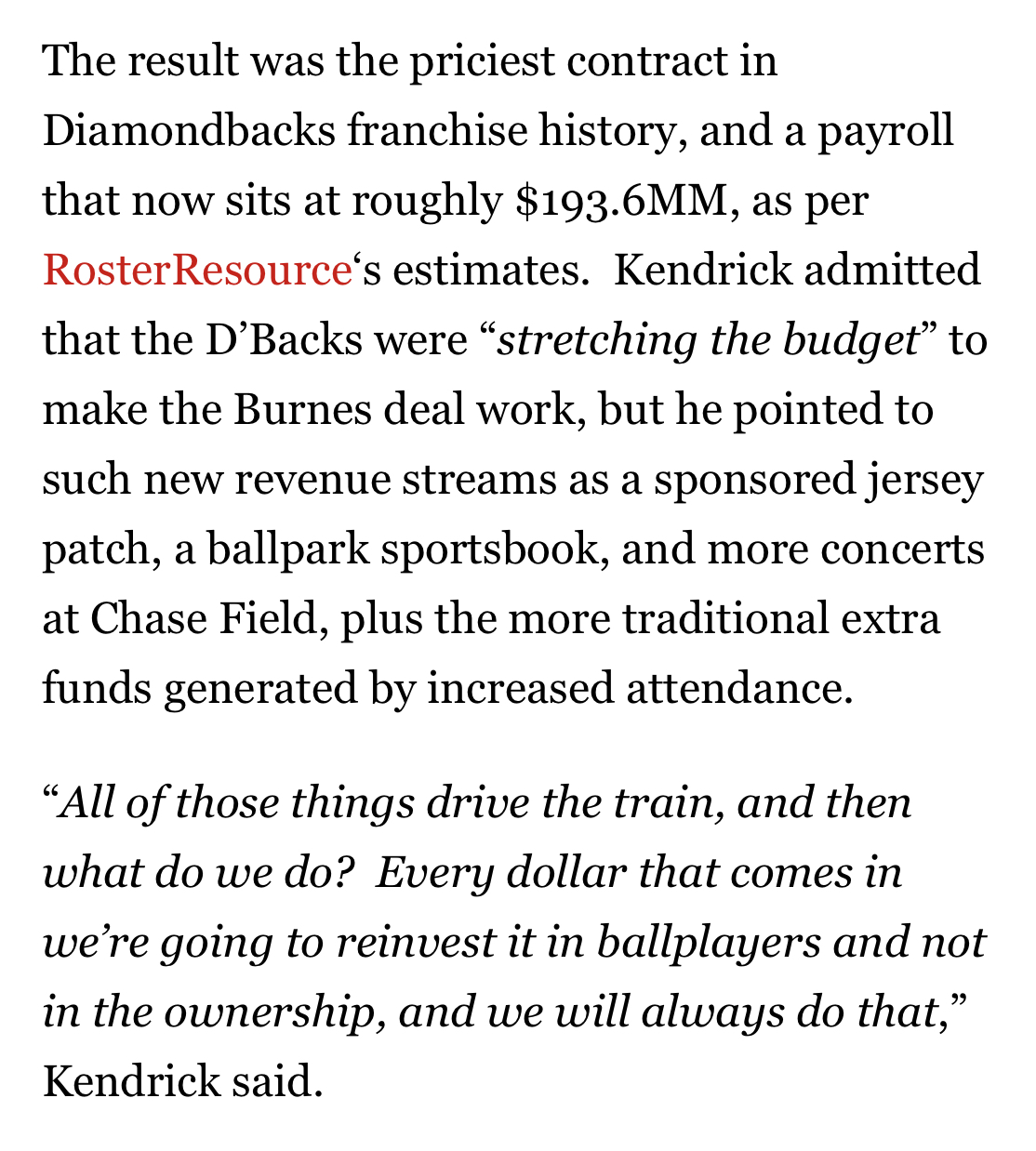

Then in December, Arizona struck, signing Corbin Burnes to a 6-year, $210 million contract, the largest in team history.

The Burnes deal was initially negotiated by Kendrick while his own Ivy-trained POBO, Mike Hazen, was out of town. Burnes wanted to be in Arizona and Kendrick decided going all-in was worth pushing past the team’s planned (and already healthy) payroll budget.

At Burnes’ introductory press conference, Kendrick stressed both a commitment to winning and the influx of new revenue, as reported by MLB Trade Rumors:

So even for a mid-market team it’s possible to leverage the club’s special status in the community for new sponsorships, creatively use the stadium for myriad events, capitalize on the gambling boom, and sign a star to drive higher ticket sales? Shocking concept.

In a trice, Kendrick blasted a gaping hole in the narrative most of his brethren have cultivated over the last decade-plus.

The Tigers have all these new revenue streams as well—corporate-sponsored uniform patches, gambling sponsorships, an in-stadium sportsbook, and Chris Ilitch leases and controls and collects revenue from events at Comerica Park (and Little Caesar’s Arena). He could even partner with a Legends to generate liquidity from a stadium ops deal, both at Comerica and LCA.

Ilitch has the resources to extend Skubal and add a game-changing free agent like Bregman.

The difference is will.

A few months ago Kendrick, a self-made entrepreneur like Mike Ilitch, bemoaned his club’s signing of Jordan Montgomery last offseason—another deal he pushed personally—but Montgomery’s disappointing season did not deter the Burnes deal. Kendrick didn’t use it as a shield to cower in the payroll shadows. Like Mike and Arctos’ Charles, he understands that reinvesting in the product only increases its value.

Detroit Is Not A Small Market And The Team Is Close (But Not As Close As You Think)

From a business and baseball perspective, now is exactly the time to extend Skubal and sign Alex Bregman, the last All Star-caliber free agent remaining on the market. We hear people talk about this “exciting, young up and coming” Tigers team. That description fits a few everyday players—Riley Greene, Kerry Carpenter, Parker Meadows. But there are a ton of holes; to wit, in the first half of 2024 Detroit had MLB’s 21st best team offense (96 wRC+). In the second half, when all the “exciting young players” were fully contributing? They ranked 20th and were actually a touch worse (95 wRC+). Trey Sweeney is a perfectly cromulent shortstop in the field but probably not with the stick. Spencer Torkelson, Detroit’s 2020 first overall draft pick, has looked alternately flawed and lost at the plate and is a poor defender. Colt Keith and Jace Jung are bat-first prospects who haven’t hit that well yet and don’t field any position well either (Keith is already being moved from second to first base).

There’s a need at least at third base, shortstop and for a right fielder who can slug; indeed Detroit ranked 20th in team isolated slugging. Yes, there’s exciting potential in the lower minors with Max Clark, Bryce Rainer and Josue Briceño, but they won’t be MLB-ready for at least two more years—and Tork stands as one of the starkest recent examples that gilded prospect status ensures nothing in terms of MLB production. That’s why you have to also strategically spend in free agency to win.

Indeed, the recently released PECOTA system projects the Tigers for 79 wins, 14% odds to win the division and 23% to make the playoffs. Perfectly average.

Bregman is also a perfect fit: an OBP machine, multi-time champion and All Star coming off his first Gold Glove at third base and quite easily the best position player free agent still available. He would immediately boost the offense, defense, solve the third base problem and bring invaluable experience to a younger team.

Teams like the Tigers, who are close but no lock to compete, benefit most from just one or two significant additions. For example, Bregman’s on-field production alone would increase Detroit’s playoff odds from 31.2% to 43.6% per FanGraphs ZiPS projections. That is easily the biggest impact Bregman would make to any team rumored to be interested in him (only the Royals would gain more at +14.6%). He doesn’t move the needle enough for the truly terrible teams and the loaded ones don’t have a need, but the impact is huge for clubs on the brink of contention.

Yet the Tigers are reportedly “waiting Bregman out” to get a discount as his market has appeared to stall.

We’re not cheap we’re sharp.

Again, in isolation trying to get better terms isn’t a sin, but despite the rumored interest and Tigers manager AJ Hinch having managed Bregman as a younger player, few Detroit fans really expect Chris Ilitch to pull this off. A slew of other established free agent hitters that would have helped Detroit long ago signed elsewhere.

And he lowballed his own Cy Young.

It’s also not expected because Ilitch clearly made a calculated decision since inheriting the team: to take advantage of MLB’s revenue-sharing model by making the team cheaper and less competitive, to go from revenue sharing payor to payee, to co-opt the Moneyball idea by pretending you are limited by a small market when in fact all those foregoing decisions could do nothing but reduce revenues—then look around, palms up, saying can you believe this, no one’s supporting this team! Why put money into the team when you know you’ll make a profit regardless, courtesy of the teams you once competed against for the best players.

Just because you can doesn’t mean you should.

It’s worth noting that despite being a recent revenue-sharing recipient, it doesn’t have to be that way for Detroit. It is not a “small market.” The city proper has not resembled the old “violent and abandoned” stereotype for many years. The larger metro area is just a place like many other places, but with four million-plus people and all the usual wealth and struggle and stratification and hipsters and militia members and an ever-compressed middle.

Metro Detroit is the 12th largest MLB metro area by population and second-largest in the Midwest, over twice the size of Kansas City and bigger than Cleveland and Cincinnati combined. Oakland County outside Detroit is one of the 10 wealthiest in the US by per capita income (min. 1,000,000 residents).

Yes, Chicago is just a five-hour drive from Detroit and the Cubs are the dominant brand in the Midwest, but the Tigers have geographic advantages many teams do not. They are the only team in a state that borders three other states and Canada. The Ambassador Bridge between Detroit and Windsor remains the busiest international border crossing in North America in terms of trade volume and value.

The city of Detroit has encouraged new tech development, and technology firms have grown there by 59% post-pandemic, compared to 30% nationally.

The metro Detroit market may be analogous to the NBA’s San Antonio Spurs, only with a larger base. Sixth Street co-founder Alan Waxman has explained why his PE firm saw opportunity with the Spurs: despite its perception as a small market, geographic and demographic factors including a burgeoning tech corridor made the Spurs “a regional team” in his analysis. Sixth Street bought a 20% stake at a $1.8B valuation. This aligns with the idea that fan passion “operates as a moat” to other revenue streams.

But you have to have a creative plan to actually grow the business and encourage belief in the community that you are trying to put the “best product on the field”—and “then brands want to be associated with it.”

And you have to want to.

Or you could run it like a corporate raider intent on slicing it up and selling out. But if you do, please do the selling.

The Duty To Give A Damn

The Seidler and Mike Ilitch legacies appeal to an owner’s vanity at minimum, which properly framed is really an intangible and not insignificant psychic good.

We have also discussed the clear economic benefits of fielding a team with at least a couple stars.

But there are broader lessons to draw from moral and even legal philosophy to support the notion that MLB owners should spend actively enough to avoid falling into the bottom of the “Scrooge” bucket, even without a salary floor/cap.

Corporations law mandates that directors and officers owe a duty of care to act in the best interests of the company. In the US we have fully acceded to the idea that the only stakeholders that matter to a company are its shareholders or owners; this “rule” has been argued to apply even to quasi-public entities like power utilities.

But it doesn’t have to be this way. In Germany for example the idea of a corporate stakeholder is broader—labor has at least one seat and vote on nearly every corporate board, and employees comprise 50% of large corporation boards.

Even here, utilities are subject to added regulation and review in most states. This is of course because everyone needs to use them and they are allowed to operate effective monopolies that would otherwise be barred by antitrust law.

Given that leagues like MLB are permitted to operate monopsonies exempted from typical business regulations due to public interest and affection, would it be so bizarre to legally designate major sports teams quasi-public entities, and to somehow give fans a voice in teams’ planning a là German workers?

Negligence law holds that each of us is bound by a duty OF care; to avoid carelessness when operating machinery, to post warnings on an electrical fence, to avoid careless acts that may injure others, and so on. The duty is based on reasonableness, i.e. what would a reasonable person do. If harm comes to another from the defendant’s action (or inaction), and they did not act reasonably, there may be liability.

In the baseball context, if you as owner receive over $100 million in guaranteed revenue annually—not to mention county stadium funding and rocketing asset valuation—that would not exist but for fans’ interest and passion, yet you consistently just skim off the marginal profits, causing fans distress, could we demand that you reasonably should spend more than 35% of revenue on player pay?

This goes hand in hand with another legal theory: one who receives a benefit from another should not be unjustly enriched at the other’s expense. We can think of few situations more in line with the spirit of unjust enrichment theory than the MLB owner who gets all the special economic and legal treatment that flows from community affection, but never really spends and instead sells fans on some indeterminate future success that never manifests.

In contracts law there is the concept of implied promises, an equitable idea related to unjust enrichment: if one party acts in such a manner as to imply an agreement exists—such as fans buying tickets and merchandise with the expectation the team will compete?—and the other party benefits from that behavior, then courts can find there is indeed a binding agreement between the two.

We are not seriously proposing that the law of contracts or negligence be directly applied to skinflint owners like Chris Ilitch through a class action or the like. It’s a loser from the start under the current order and norms. But while sports fandom may be unreasonable, could we turn an analogous phrase to the duty of care: owners should be held at least to a basic duty TO care. You have a captive customer base that you did, in some cases, almost nothing to cultivate. The “reasonable” response would be to act like you give a shit.

Moral philosophy, whether Kantian or utilitarian or simple common sense, recognizes that special obligations exist for an agent (the owner) relative to those with whom he or she has a special relationship, e.g. friends, loved ones, intimates.

Fans are, in a very real way, intimates of sports teams relative to other business relationships—we are raised to root for local teams and give inordinate time, money and care to them. It is hard-wired. The fans’ affections and behavior, including misery and suffering, embody expectations that the team is trying to win, and the team’s real value derives from these affections, hence one could argue that the owner has a moral duty to alleviate that suffering, just as one would for a relative or friend.

If we strip away moral questions and “should’s” altogether, MLB’s antitrust exemption flows directly from the special relationship between fans and that industry. Why does the legal exemption continue in perpetuity when 2/3 of the league abuses the standing that created it in the first place?

A more direct solution would be MLB itself changing its standards and incentives. Could it better vet potential owners and have standards for continued inclusion in its exclusive club? Why not directly enforce the rules for revenue-sharing recipients to spend a higher threshold on players, and then penalize the laggards in lottery picks and revenue sharing bucks to ensure they follow through to actually try to spend, improve, win? If you can’t commit to reinvest 60% of baseball revenue into players on a team you just purchased or inherited, you are out within three years?

What about performance standards. If you draw less than 50% home capacity for five consecutive years you must sell and are forced to X out that precious spreadsheet page? Players who fail on that level are dumped far quicker.

Can MLB set a higher standard of unaffiliated wealth, i.e. make Steve Cohen-level assets the median not the outlier for new owners, even if it means prioritizing investment groups over a single general partner?

We are casting about for answers that do not come easily. Another way to approach this question is to find solutions to the purported problem underlying payroll stinginess; that these teams don’t have enough money.

There is a notion that sports teams can only grow revenue so much, that they are restricted by geography in ways other businesses are not. Of course there’s some truth here, but a simple answer is that guaranteed revenue streams should not be treated as both floor and ceiling. That revenue base of $100M+ should be a springboard, not a straitjacket. We have covered some of the ways teams could improve revenue. Work out new and additional media arrangements via social and streaming. Develop the land you control around the stadium. Consider owning or co-owning your own local broadcasting like the Yankees and Dodgers—and now the Rangers, who recently decided to develop and operate their own RSN. Develop fresh marketing and merchandise, which is of course easier to build around star players.

Bring in private equity liquidity and expertise to offset payroll costs. There are tens if not hundreds of millions available for a fraction of ownership, or of interest in secondary functions like stadium ops and media rights.

The sports ownership club is also supposed to be rarefied air; it shouldn’t be the end-all means to pay for your groceries. Or pizza toppings. Only allow owners in who are committed to operate as D’Backs owner Kendrick and the Arctos guys emphasized: players and a competitive team must drive everything.

In other words, just as any other viable business must do, put something in to get something out.

But as things stand now, owners don’t have to do any of that because the floor and guaranteed profit is there regardless, not to mention the ineluctable rise in team values. Mike Ilitch bought the Tigers for $85 million in 1992. If Chris were to sell today he could fetch an estimated $1.4 billion.

Humor us, though: how much would it be if he had Skubal—homegrown and developed—locked up long term plus one or two other All Star type players? Certainly not less.

May As Well Be The Desert Cats

Again, baseball teams are not widget or pencil or pizza companies. They are unique assets: baseball is entertainment, but more than that, communities follow and spend on sports teams across decades out of a loyalty they aren’t going to feel to a brand of toilet paper or microchips or even a local restaurant after the food or service goes bad.

If one has the privilege of owning an asset this bulletproof as a result of public trust, it should come with an expectation and obligation to make it good, to make it compelling, to make it competitive. The reality of antitrust exemptions and guaranteed revenues flows from the understanding that this is a social artifact, a thing people care about in ways unreasonable and wonderful.

A baseball team’s cultural significance makes it too big to fail.

You can operate that thing like the odd acquisition you plunder and flip, but you shouldn’t. Or if you are running it that way, at least do the damn flipping—sell it for a billion dollar profit to someone with the spirit of Mike Ilitch or Peter Seidler.

Hell, there is surely a random Saudi prince who loves the Tigers at least as much as Chris Ilitch seems to, and wants to compete much more.

Mike Ilitch paid for stars. The team was a contender. Ticket sales and revenues went up. Fans were excited and literally invested.

His son didn’t learn those lessons. Chris doesn’t spend on players. He isn’t creative about marketing the team. He hasn’t had to build anything. He hasn’t had to put anything into anything—whether pizza or property or baseball—to achieve vast wealth.

So instead he rolls out Scott Harris with only a flak jacket bedazzled with spreadsheets and pepperoni and vague assurances that at some distant time they will spend. So instead hey look over there, a “youth movement.” So instead hey look over here, we built a new weight room and finally removed the ashtrays from the team plane.

So instead hey we kinda tried but please blame Boras if we lose the 27 year old Cy Young winner grown in our own backyard.

You can do all that.

But should you?

Fantastic read here.

The most widely spread mistruth in sports is that baseball owners are all about profits. They are not. In fact, like you discussed, I believe the opposite. If we're speaking in terms of total profits over the lifetime of the owner, MLB owners like Chris Ilitch actively work against their own interests, by instead choosing to consistently operate the team in a way that maximises profit realised today, then taking that same strategy tomorrow, and every day, infinitely. Paradoxically, maximising profit on each individual day is not the way to maximise lifelong profit, so I can definitively conclude that MLB owners are not strictly in the business of maximising profits.

This is why the teams that have private equity behind them, who are ACTUALLY profit maximisers, tend to splurge for FAs, while the traditional owners are the cheap ones.

As you brought up, MLB owners operate their teams as if they are assets that are about to be flipped, with the absolute deference to immediately realisable profits, but they never actually flip them. This raises the question of why these teams operate this way. If you plan to hold onto the team (as Chris Ilitch has done), why spend the last eight years operating as if the team is one month from being sold?

It's hard to know the answer to that question. There's always the Soccernomics explanation (that sports to these owners are small apples in revenue terms, allowing for more inefficient business behaviour). In English, this is basically accusing baseball owners of not running their teams well, because even if revenue (not profit, just revenue) goes from $400M to $500M, that is still chump change to them. Most baseball owners are involved with businesses that can double that number at least every year. Perhaps in those other businesses, they feel the need to profit maximise, just not in baseball, because the money (relative to the other business interests of a billionaire baseball owner) is still so small.

That's one explanation. Another is just that these owners that have inherited the teams they run are just idiots that don't know how to profit maximise. Chris Ilitch didn't build Little Caesar's after all. Mike did that. All Chris has to know how to do is not run the business off a cliff. This explanation could explain why the self-made entrepreneur type of owner is consistently better at it than the son/daughter who inherited the team type of owner.

Now that we've confirmed that the owners are not adequately profit maximising, the buck falls on baseball itself. Why is this allowed?

Baseball has gone a long way towards fostering this culture of 'efficiency,' largely (in my opinion) in an effort to reduce leaguewide payroll. Big playoffs (allowing one more cheapskate team like Detroit in every year) moved the game in this direction, the increased draft choice disincentive to sign FAs moved the game in this direction. There are other things I can bring up. I won't name them all, but it's clear that baseball itself (the league office and the league culture) likes this direction, despite it neither being the profit maximising strategy nor the entertainment maximising strategy. This is why rules around ownership will never change to lessen this kind of behaviour. Why would they do that when ever since Rob Manfred became commissioner, they have consistently been changing rules to encourage this kind of behaviour?

Why is that?

Quite honestly, your guess is as good as mine. I don't know why baseball wants things to be this way. I don't know why the league office aided in this effort instead of pushing back against it. I don't know how the promise of winning more games while not making any less money consistently fails to push owners to the so-called dark side of actually trying to win. I don't want to call everybody involved an unintelligent human who either doesn't know or doesn't care how to maximise their own money, but what other choice do I have? What other rational explanation is there?

Like you said, if these teams ever actually got sold, this behaviour would make some sense, but since they never do, why operate a baseball team like an investment asset that you're hot to get off of?

I can't answer that.

Passionate and intelligent. Well done!